Definition

Skew is the relative richness of put vs. name choices, expressed by way of Implied Volatility (IV). For choices with a selected expiry, 25 Delta Skew refers to places with a delta of -25% and calls with a delta of 25% to reveal this distinction out there’s notion of implied volatility.

25 Delta Skew is calculated because the distinction between a 25-delta put’s implied volatility and a 25-delta name’s implied volatility — normalized by the ATM Implied Volatility.

Whereas Implied Volatility is the market’s expectation of volatility.

Fast Take

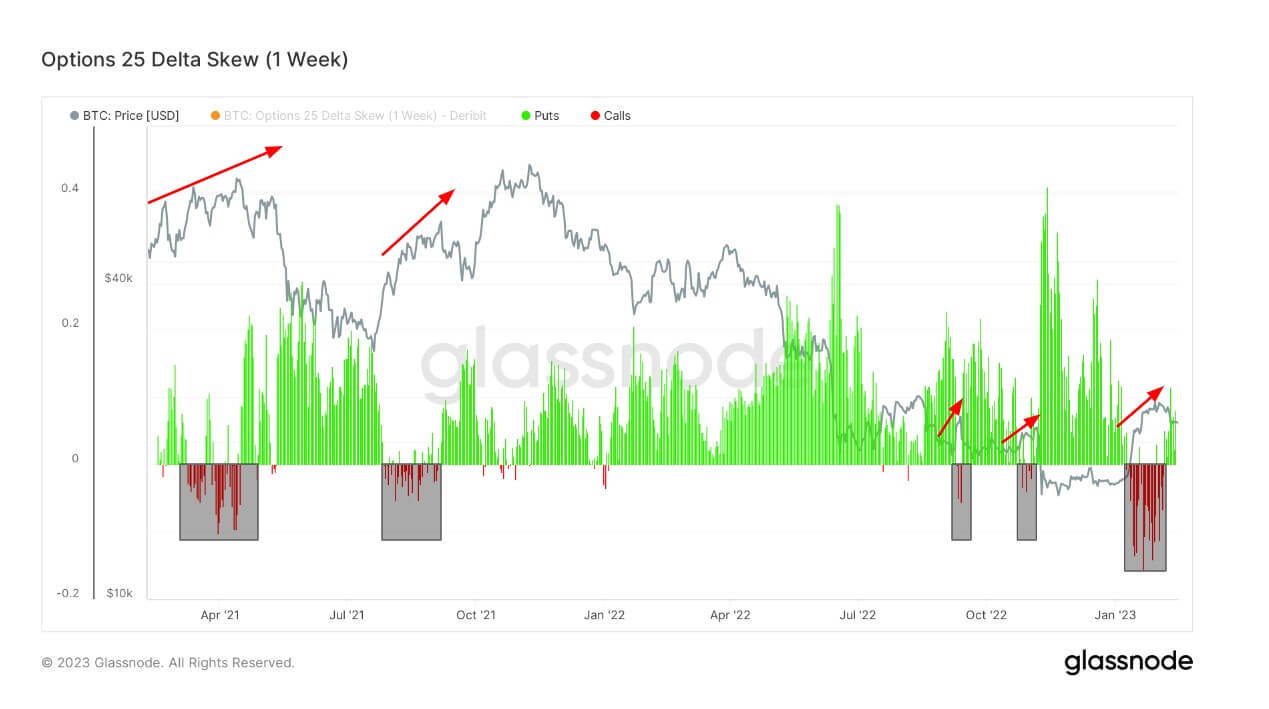

- Choices 25 Delta Skew suggests places are dearer than calls — indicating bearish sentiment forward of the CPI announcement right this moment.

- For the previous two years, every time calls develop into dearer than places highlighted within the black field, Bitcoin has a rally in value — doubtlessly indicating a bear market rally.

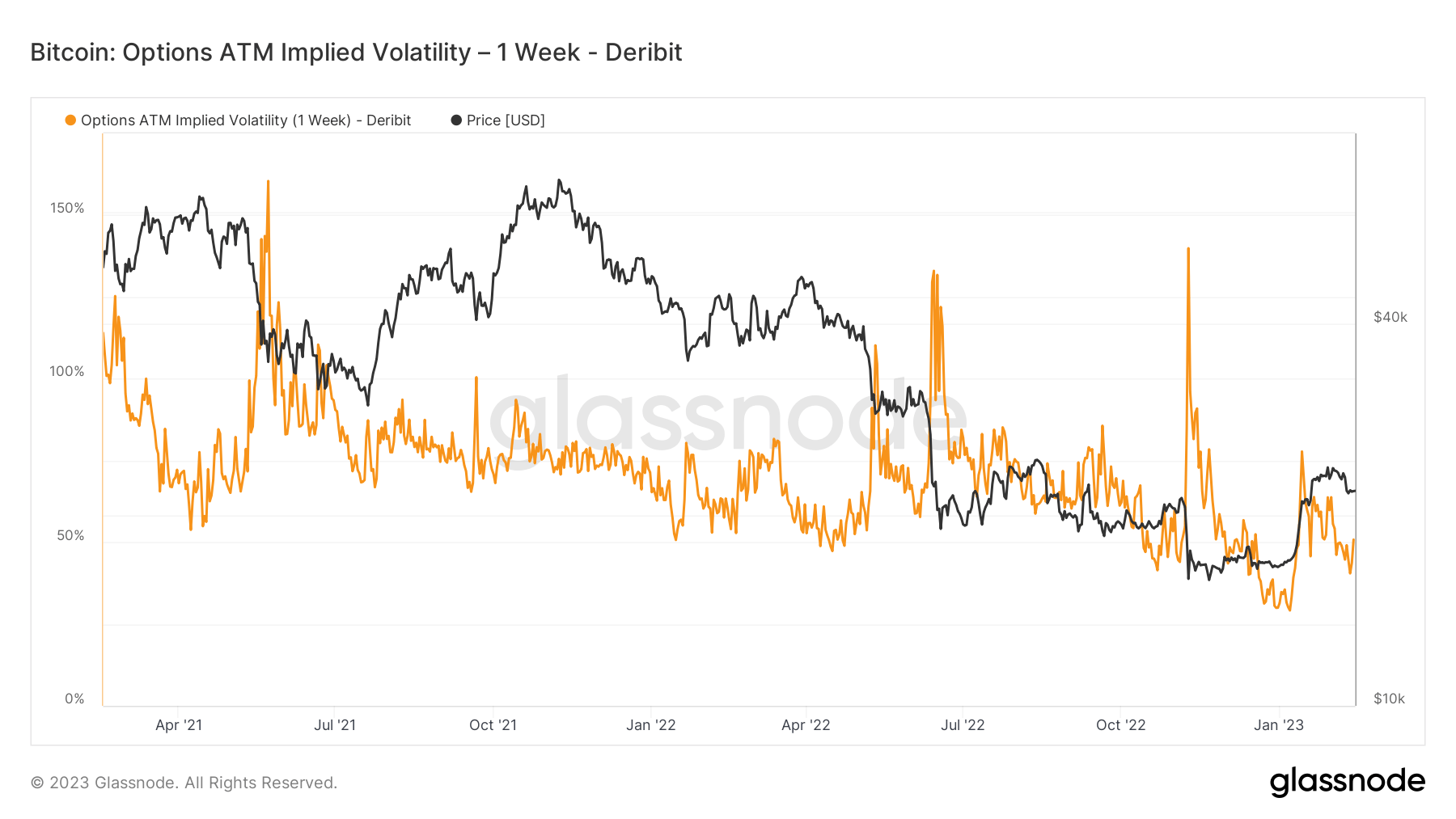

- Implied volatility has come down meaningfully because the FTX collapse, at the moment at 50% — versus 140%.

- 25 Delta Skew and implied volatility give attention to choices contracts expiring in a single week from right this moment.

The put up Choices 25 Delta Skew suggests bearish sentiment forward of CPI appeared first on CryptoSlate.